2026 Estate Planning Update

Estate Tax Update

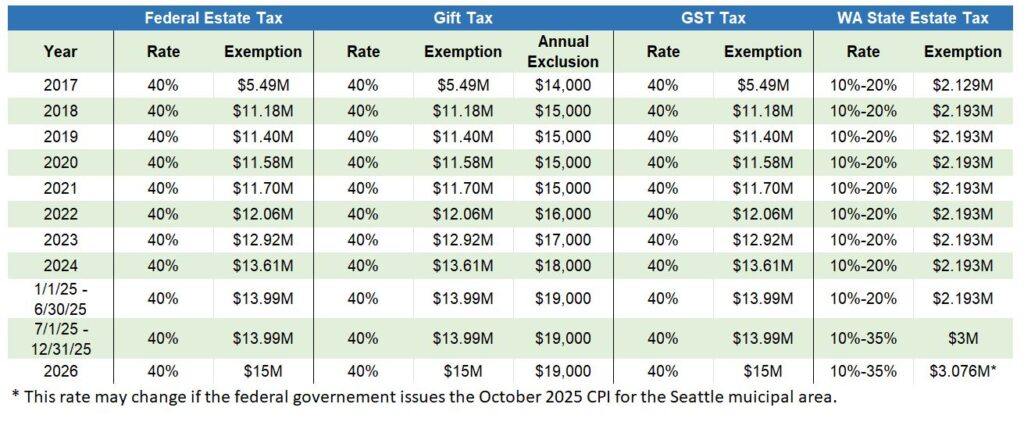

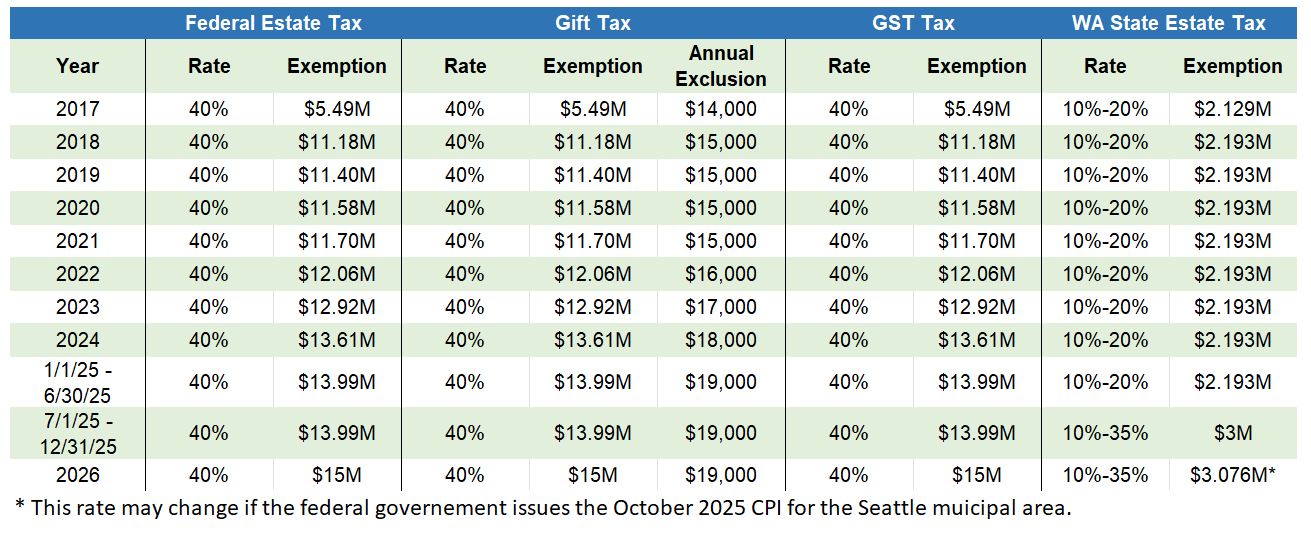

FEDERAL ESTATE TAX, GIFT TAX, AND GENERATION-SKIPPING TAX EXEMPTIONS

The 2026 federal exemption against estate and gift taxes is $15,000,000 per person. This is an increase over the 2025 exemption, which was $13,990,000 per person. Gifts and estates in excess of the exemption amount are subject to a 40% federal estate tax. The federal generation-skipping transfer tax exemption was also increased to $15,000,000 per person.

STATE ESTATE TAX EXEMPTION

After years of holding the Washington State estate tax exemption at $2,193,000, on July 1, 2025, the State legislature raised the exemption to $3,000,000 per person beginning July 1, 2025, with inflation adjustments each January thereafter. However, due to the federal government shutdown during October 2025, the U.S. Bureau of Labor Statistics has still not issued an October 2025 CPI for the Seattle municipal area, which is the CPI that Washington uses to adjust its estate tax exemption. Currently, Washington is relying on the August 2025 CPI for the Seattle municipal area and declaring an inflation adjusted estate tax exemption for 2026 of $3,076,000. However, they have reserved the right to adjust this amount if the federal government issues the October 2025 CPI.

Together with the increased exemption, the Washington State legislature also increased its tax rates. Washington estates in excess of the exemption amount are now subject to a 10% – 35% tax (previously, the top bracket was 20%).

FEDERAL GIFT TAX ANNUAL EXCLUSION

The federal annual gift tax exclusion is $19,000 per person, per donee. This is the same rate as it was in 2025.

FEDERAL AND STATE TAX SUMMARY

The chart below outlines the federal and state exemptions and tax rates for 2017 through 2026.

{kind=link}

GIFT TAXES – E-FILING IS AVAILABLE!

The Internal Revenue Service has recently implemented a significant modernization to the federal gift tax filing process. They anticipate that beginning in 2026, federal gift tax returns (Forms 709) may be filed electronically. For years, taxpayers and preparers have been limited to paper filing for gift tax returns, even as most other major tax documents moved to e‑filing. This change reflects the IRS’s broader effort to streamline tax administration, improve accuracy, and reduce processing delays.

E‑filing gift tax returns offers several practical benefits. Returns submitted electronically are acknowledged instantly, helping taxpayers confirm receipt and avoid uncertainty about whether their return arrived on time.

From a planning perspective, this change can be especially valuable for the estates of high‑net‑worth individuals. With e-filing, it should be easier and faster to obtain transcripts of e-filed returns, making it easier for Executors who are required to attach copies of all gift tax returns filed during a decedent’s lifetime to the final estate tax return. It will also eliminate the need to prove to the IRS that a return was timely mailed.

WASHINGTON STATE CAPITAL GAINS TAX UPDATE

Washington’s capital gains tax, originally enacted in 2021, imposes a levy on long-term capital gains realized by individuals and certain owners of pass-through entities from the sale or exchange of stocks, bonds, business interests, and other investment assets. The tax applies to gains allocated to Washington State and is separate from federal capital gains tax; it generally does not apply to real estate sales or assets held in certain qualified retirement accounts.

For tax years beginning after January 1, 2022, Washington implemented a 7 percent excise tax on long-term capital gains above an annual standard deduction (adjusted for inflation). In 2024, the standard deduction was $270,000. In 2025, it increased to $278,000. As of the date of this article, Washington has not published its 2026 standard deduction.

In response to ongoing budget pressures, the Washington Legislature adopted ESSB 5813, which added a tiered tax rate structure effective for tax year 2025 (returns due in April 2026). Under the new system, gains in excess of the exemption and up to $1 million are still taxed at 7%, but gains above $1 million are now subject to an additional 2.9% excise tax, bringing the top effective rate to 9.9%.

This rate increase took effect retroactively to January 1, 2025, meaning that transactions occurring earlier in the year will be subject to the new tiered structure when taxpayers file in 2026.

The law includes specific exemptions and deductions: (1) the initial exempt amount (the standard deduction referenced above), (2) deductions for qualifying charitable donations, and (3) deductions for gains from the sale of qualified family-owned small businesses, subject to limits and definitions.

Capital gains tax collections have become a significant revenue source for education funding, with recent reports noting collections exceeding $560 million in 2024.

NEW REAL ESTATE DISCLOSURE REQUIREMENTS

Starting March 1, 2026, the anti-money laundering regulations for residential real estate transfers, which is administered by the Financial Crimes Enforcement Network (FinCEN), becomes effective. FinCEN has identified certain real estate transactions, especially those conducted with cash outside of the banking system, as high-risk for abuse by illicit actors. The purpose of these new regulations is to improve transparency and combat money laundering, terrorist financing, and other illicit financial activity in the U.S. residential real estate market.

Who Must Report. Certain professionals involved in real estate closings and settlements, such as title agents, attorneys, and settlement agents, are required to submit a Real Estate Report to FinCEN. This reporting obligation applies only when the purchaser is a legal entity or trust, not an individual.

What Transactions Are Covered. The rule targets non-financed transfers of residential real estate (typically all-cash deals) where the buyer is an entity (e.g., LLC, corporation) or a trust. The rule applies nationwide and covers single-family homes, townhouses, condos, co-ops, and similar residential properties, even if part of a larger mixed-use building.

What Information Must Be Reported. The Real Estate Report requires detailed data about the transaction, including:

- identity and contact details of the reporting person (the professional filing the report),

- identification of the property and transferor,

- information on the transferee entity/trust,

- beneficial owners of that entity/trust (those with significant ownership or control),

- transaction value and payment details.

When Reports Are Due. Reports generally must be filed within the later of (a) 30 calendar days after the closing date or (b) the final day of the month following the closing of the transaction. FinCEN has published a standardized Real Estate Report form for this purpose.

Compliance Timing. The new reporting rule was originally slated to start on December 1, 2025. However, FinCEN has postponed compliance until March 1, 2026.

ESTATE TAX RELIEF BY CHANGING RESIDENCY: WHAT WASHINGTON FAMILIES SHOULD KNOW

Washington imposes a state estate tax on decedents who are domiciled in the state of Washington at the time of death. Under current law, the state estate tax exemption is approximately $3 million (indexed for inflation), with tax rates ranging from 10% to 35%. This means that estates exceeding the exemption can owe significant Washington estate tax before any federal estate tax is due.

One approach for high‑net‑worth individuals seeking to reduce or eliminate Washington estate tax exposure is to change domicile to another state that does not impose an estate tax (e.g., Florida, Texas, Nevada, Wyoming, Alaska, or South Dakota). In such states, decedents are only subject to federal estate tax on amounts in excess of the $15 million per person exemption. Changing domicile can therefore save a taxpayer significant amounts.

However, simply spending time out of state or owning property elsewhere does not eliminate Washington estate tax. For estate tax purposes, the key concept is domicile — your “permanent legal home” that you intend to return to and remain in indefinitely. Washington’s rules for determining domicile align with general tax and legal principles: domicile depends on intent and actions rather than just physical presence. To change your state of domicile, you must demonstrate both physical residence in the new state and a genuine intention to make it your permanent home.

Practical steps typically used to establish a new domicile include (but are not limited to):

- Spending a majority of your time in the new state and maintaining a primary residence there;

- Selling or otherwise reducing ties to your Washington home (e.g., not treating it as your primary residence);

- Registering to vote in the new state;

- Obtaining a driver’s license and vehicle registration in the new state;

- Changing mailing addresses, banking relationships, and professional affiliations to the new state;

- Filing state income tax returns (if applicable) in the new state rather than Washington; and

- Demonstrating social, business, and community ties in the new state.

Even after establishing new domicile, Washington may still tax a portion your estate if you continue to own Washington real estate or tangible personal property in your own name at death. In that case, Washington may treat those assets as Washington‑situs for estate tax purposes and may require an apportionment of tax attributable to the Washington property. This means that while changing domicile can eliminate full estate tax on personal property and intangible assets, real estate located in Washington might still generate state estate tax liability for non‑residents.

Because domicile is fundamentally determined by facts and circumstances, taxpayers relocating for estate tax reasons should take a comprehensive and documented approach to establishing their new residence. A cohesive plan that includes updating legal documents, changing registrations, reallocating personal and financial ties, and aligning lifestyle behaviors with a new home state helps support the intended change in domicile.

In sum, moving out of Washington can be a powerful estate tax planning strategy for certain families with significant estates, but it requires more than a casual change of address. The difference between residency and domicile — and the implications for estate tax — underscores the need for careful planning with legal and tax advisors.